4. Case Studies

4.1 The Case of Malaysia and Indonesia: Rethinking Biofuel Policies for Sustainability and Flexibility

Lead Author: Chun Sheng Goh, Jeffrey Sachs Center on Sustainable Development

In Malaysia and Indonesia, the use of local bio-resources for energy purposes is not only perceived as an option to ease the stress of energy security but also an opportunity to create new jobs and income for farmers and the general rural population. Most of the time, the latter is perceived as a more important motivation for biofuel development as both countries are in fact large oil and gas producers. Initially in the 2000s, biofuel development was championed by trade and investment departments. Ambitious, mega-scale targets were set without carefully considering the vital links between economic, environmental, and social elements. Later, both countries gradually adjusted their targets to recognise that biofuel development needs to cover combinations of policy interventions across multiple sustainable development goals, especially economic growth (SDG 8), industrialization (SDG 9), energy (SDG 7), climate change (SDG 13), land-use (agriculture and forestry) (SDG 2 and SDG 15) and rural development (SDG 8). Evaluating the role of biofuels in achieving sustainable development in these countries would require more holistic thinking beyond just 'land' or 'energy' and instead covering multiple aspects of a place or territory. Evaluating the sustainability of biofuels in these countries, therefore, must carefully consider the regional and local context.

4.1.1 Palm Oil

Palm oil is the major cash crop in Malaysia and Indonesia. The palm oil industry, following the rubber industry, was developed as a means to jumpstart the economy in many parts of the countries. It plays a key role in economic development, contributing a significant percentage of the countries' revenues. A dominant feature of the palm oil industry is the extent to which exports of primary products, i.e. crude and refined palm oil, still loom large. However, due to a scarcity of suitable land resources and labour forces, Malaysia has lost its comparative advantage in furthering oil palm expansion. In Indonesia, the unsustainable mode of oil palm expansion has also greatly increased risk of environmental degradation and social conflicts. In the next few decades, it is unlikely that both countries will continue to see similar low-cost expansion as in the past due to biophysical, economic, and social factors.

4.1.2 Downstream Development

Historically, countries would pull out of low-cost, unsustainable land exploitation when they were able to diversify away from primary production. As incomes from downstream expand, land-based economies likely enter a transitional period towards more advanced, and possibly more sustainable forms of development, gradually reducing the rate of resource exploitation. As such, creating new added value through developing, upgrading, and diversifying the value chain is deemed an essential move to secure long-term economic interests. This has been regarded as a key step to transform Malaysia and Indonesia from primary producers to advanced bio-economies, as well as a turning point to relieve the countries from rampant timber extraction and agricultural expansion while improving the welfare of local population. Moving the local industries up in the commodity value chain requires advancement in manufacturing technologies, with products spanning from base oleo like fatty acids to end products like polymer and cosmetic products, and possibly in the future high- end products from advanced biorefineries. Biofuel is among the low hanging fruits in the eyes of producers as it involves relatively less complicated processing technologies.

However, there are still concerns over sustainability of the palm oil industry in attempts to move from primary production to secondary development. In the past, oil palm is often labelled as the culprit of extensive land-use change that involves massive carbon stock loss. Many organizations or movements, especially in Europe, have advocated excluding palm oil from the market, translating into policies or actions such as the 'No Palm Oil' label in France and Belgium. Among the different palm-based products, palm-based biofuels probably received the most criticism, involving numerous debates, discussions, research, movements, and even legal actions.

To better understand the sustainability of palm oil biofuels, it is necessary to place the discussion in different contexts.

4.1.3 Scale

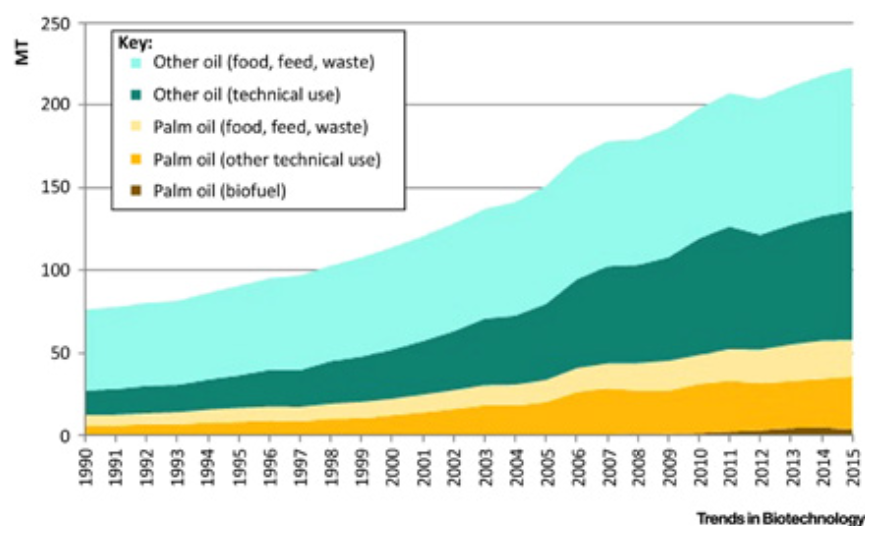

First, it is important to understand the scale of biofuels in the context of the vegetable oils market. Figure 1. shows the trend in the global consumption of vegetable oil for technical purposes (i.e., not food or feed) in comparison to its other uses. In 2011, about a quarter of the global vegetable oil demand was fulfilled by palm oil, and about two-thirds of the total palm oil was used for technical purposes. Most of this palm oil was consumed in the chemical industry, with a relatively small amount devoted to biofuel production.

FIGURE 4.1 Amount of Vegetable Oils Consumed Globally

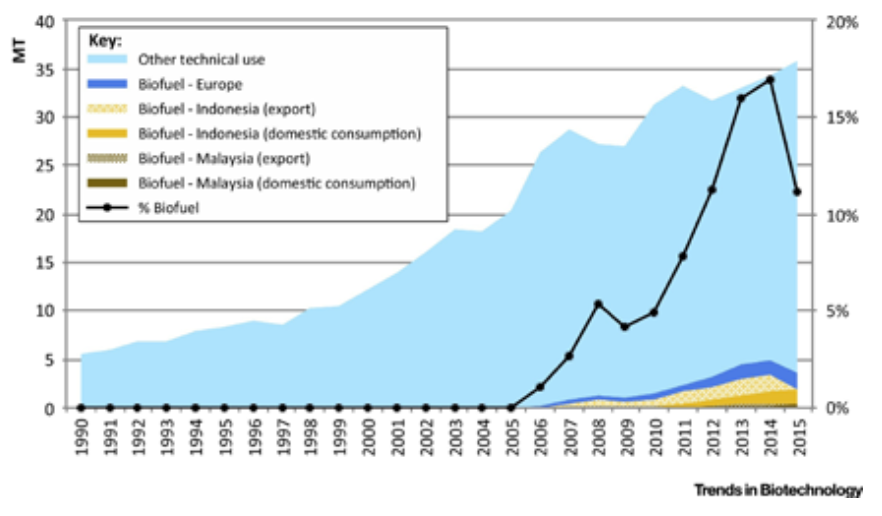

Figure 4.2 illustrates the use of palm oil for biofuel and other technical purposes. Palm oil has been used for biofuel production since 2007, especially in Europe. Indonesia and, to a lesser extent, Malaysia have historically produced palm-based biofuel for export purposes until they started to create domestic markets in 2011. In 2014, domestic consumption in these two countries had reached about half of what is consumed in Europe, while there was a sharp fall in Indonesian exports due to antidumping duties imposed by the EU. Outside of the biofuel industry, palm oil is actually much more widely used in personal care and cosmetics products, as well as in pharmaceutical ingredients. In fact, the volume of palm oil used for these purposes is more than six times that used for biofuel. Based on these figures, at first glance, the impact of palm-based biofuel is likely much lesser compared to other end-uses considering the scale of the market.

The scale of palm-based biofuel reflects that the biofuel policies in Malaysia and Indonesia are designed in a way to create a buffer for their primary commodity, i.e. palm oil. They carry the objectives of artificially creating a domestic biodiesel market for excessive stock of CPO resulting from the fluctuating prices. This is especially important in certain years when the demands for palm oil and palm-based products drop substantially.[1] Although emission reduction was often emphasized, the current domestic biodiesel market functions more as a back-up for the oil palm industry, providing more economic flexibility, especially considering that both countries are also major petroleum producers. This is also a reason why the palm-based biofuel industry in both countries is unstable, as the primary objective is to supplement the palm oil industry and less about emission-reduction or energy security. Recognising the practical challenges, governments have adopted more flexible approaches in setting blending targets, avoiding making ambitious goals for energy security and emission reduction. The competition between food and technical uses, when taken in this context, may be less of a concern.

FIGURE 4.2 Amount of Palm Oil Consumed Globally for Technical Purposes

4.1.4 Under-Utilized Low Carbon Land

Moving upstream, when biofuel production involves the use of under-utilized land, the risk of food-vs-fuel must be carefully evaluated. In reality, many idle, non-forested, and low carbon lands will remain unused for food production with or without biofuel development. This involves complex interactions between economic, agricultural, and international trade policies as well as food markets and distribution mechanisms. In many places, the incentives from biofuel production are perceived as a key to activate these land resources for productive use, thus providing new income sources for local communities. Multiple studies show that there is still plenty of non- forested, degraded land in Indonesia that remains under-utilized.[2]

4.1.5 Deforestation

Encouraging the use of under-utilized, low carbon land resources with the right incentives and rules may also prevent unsustainable expansion and conversion of forests. On a landscape scale, the new income provided by biofuel production may contribute to sustainable agrarian transitions in developing countries like Indonesia. While legislation and subsidies could protect the remaining forest, alternative funding and long-term income sources for local communities, e.g. provided by biofuels, are needed as an additional safeguarding measure. Potentially, this may be combined with incentives from the carbon tax or credit system for both land carbon restoration and emission reduction. Such combinations are still largely missing today, despite some small-scale experiments.

4.1.6 Land Availability and Readiness

Accompanying risks must also be properly understood in different regional contexts. Various names e.g. 'abandoned', 'degraded', and 'marginal' land, have been proposed to quantify land available for future expansion depending on local interpretation.[3] Their definitions or criteria may be different, and some are not entirely clear, e.g. abandoned land is not necessarily degraded, and vice versa.[4] A study by Gibbs and Salmon shows that global estimates of 'degraded' land based on different databases and methodologies can vary widely from 1 billion ha to over 6 billion ha.[5] Furthermore, the conditions of land may change significantly from time to time, complicating the monitoring efforts. At the moment, high-resolution monitoring on a landscape scale is still too costly to be implemented. On this basis, it is crucial to understand how future expansion can take place on these lands considering the multiple factors and perspectives of various stakeholders. Importantly, mobilization of under- utilized lands needs to be safeguarded from unwanted environmental impacts, with measures like regulations or market-based voluntary sustainability standards.

4.1.7 Socio-economic Factors

Furthermore, adversarial relationships between local communities, private companies, and governments, especially in terms of land rights, have been frequently cited as one of the most serious problems discouraging land development in developing countries. Navigating a biofuel production system characterized by small-scale farming is ongoing, but strong external interventions are required to protect and support such a system, as well as regulate and ensure the sustainability of the entire landscape. Importantly, the development plan must consider how the different types of land-use -- from small household mixed farming to industrial monoculture -- can co-exist and interact.

4.1.8 Final Remarks

In short, the general impressions of food-fuel competition and indirect land-use impacts may turn out to be very different by countries or regions. The potential risks mentioned above may also be mitigated with better policymaking, business model designs, and law enforcement. In the era of digital revolution, the emergence of new technologies like real-time monitoring of landscape and bioremediation of degraded soils may make biofuel production more sustainable. These provoke decision-makers to rethink the role of biofuel development from a broader perspective. Importantly, it must be placed in a wider canvas of sustainable development that cuts across multiple SDGs beyond individual sectors, disciplines, institutions, and countries. The best outcome may only be achieved through co-learning and co-design among all stakeholders across sectors and scales, capitalizing on the synergies generated from integrating various transformative strategies across sectors.

Points for policy discussion:

More holistic thinking beyond just 'land' or 'energy' but covering multiple aspects of a place or territory.

One objective is creating new added value through developing and upgrading downstream diversification to relieve the countries from rampant timber extraction and agricultural expansion while improving the welfare of the local population.

More flexible approaches in setting the blending targets, avoiding making ambitious goals for energy security and emission reduction.

Encouraging the use of under-utilized, low carbon land resources with the right incentives and rules may also prevent unsustainable expansion and conversion of forests.

Understand how future expansion can take place on under-utilized, low carbon lands considering the multiple factors and perspectives of various stakeholders.

Importantly, mobilization of under-utilized lands needs to be safeguarded from unwanted environmental impacts, with measures like regulations or market-based voluntary sustainability standards.

Consider how the different types of land-use -- from small household mixed farming to industrial monoculture -- can co-exist and interact.

The emergence of new technologies like real-time monitoring of landscape and bioremediation of degraded soils may make biofuel production more sustainable.

4.2 The Case of Brazil: Evidence that Sustainable Biofuels are an Effective and Immediate Solution for Decarbonizing Transport

Lead Author: Prof. Luiz A Horta Nogueira, Universidade Federal de Itajubá

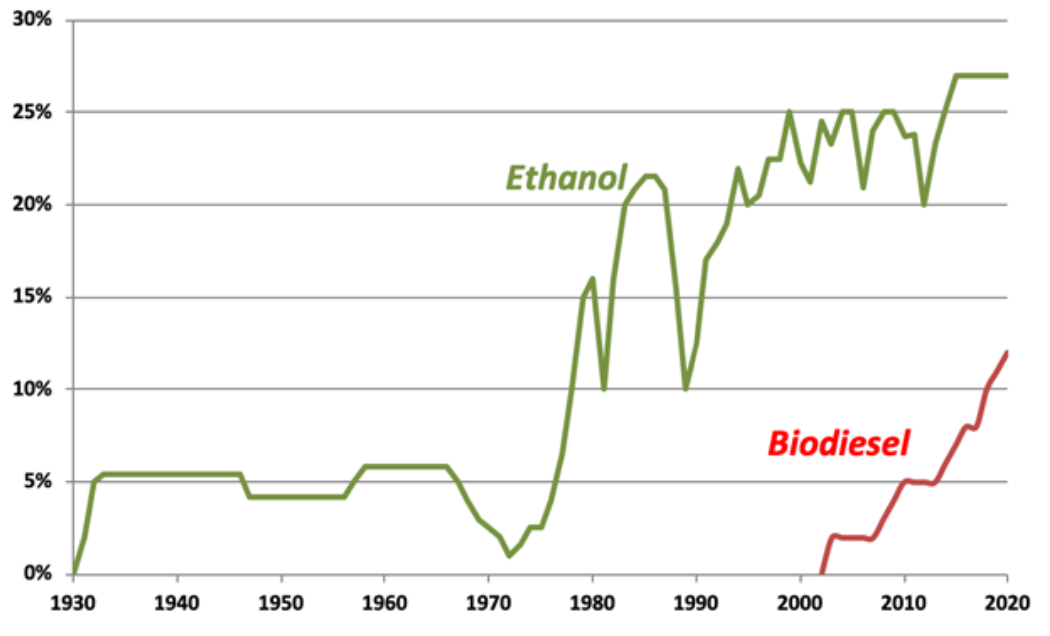

Starting with ethanol blending mandates in gasoline in 1931, Brazil has been undertaking a long and persistent journey to successfully displace fossil fuels with biofuels. Biofuels are currently distributed in all the 41,700 gas stations in the country, in the form of gasohol (E27), pure hydrous ethanol (E100) or diesel/biodiesel blend (B12). The volumes are enough to displace about 600 thousand barrels of oil per day, thereby avoiding the emission of 69 million tonnes of CO2 per year. All Brazilian vehicles (i.e., more than 47 million units), from motorbikes to heavy trucks, use some type of biofuel, either neat or in blends with oil products. The local production of these biofuels reduces energy imports, improves the national energy security, and brings social and environmental benefits.

4.2.1 Current Status of Biofuels Production and Use

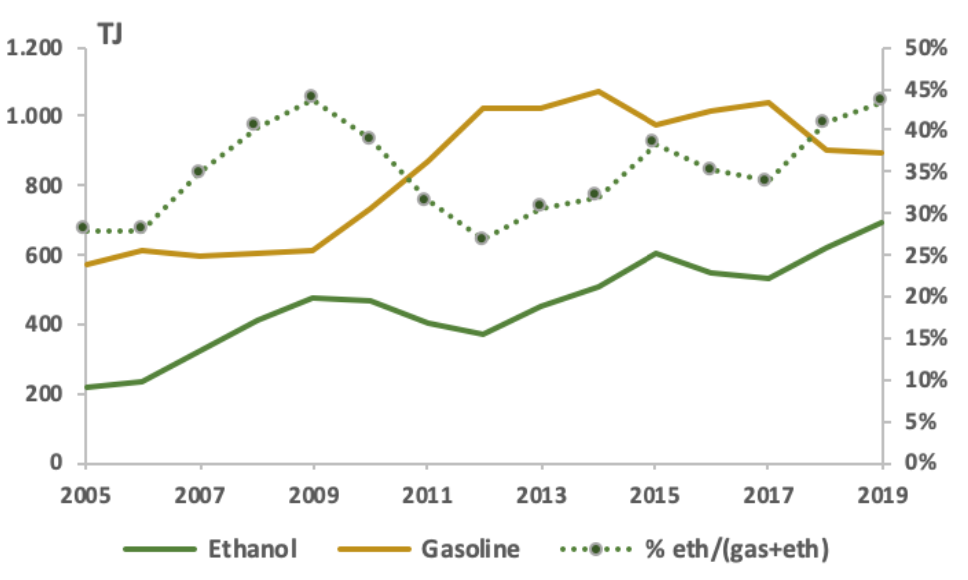

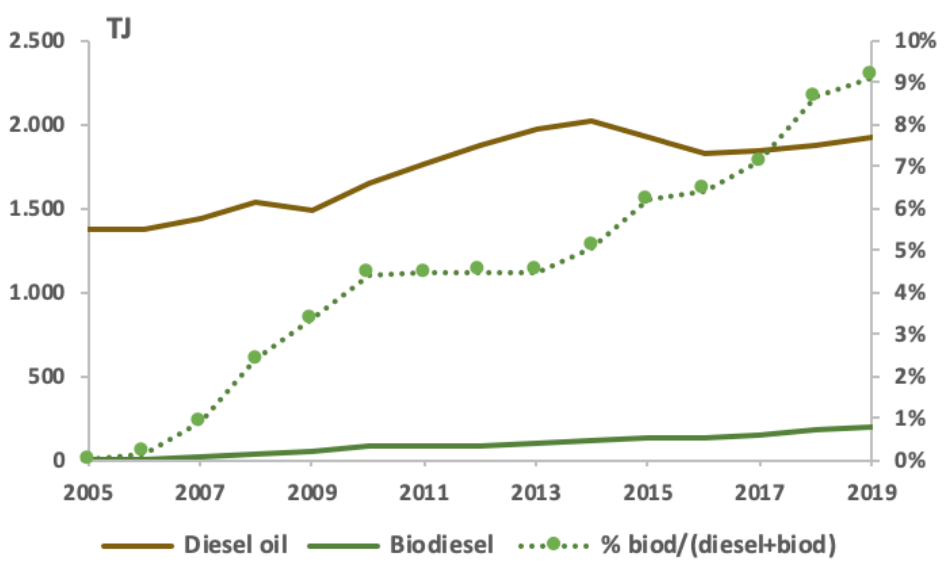

Figure 4.3 presents the evolution of blending mandates of biofuels and Figure 4.4 presents the progressive contributions of biofuels, in energy terms. In 2019, ethanol replaced 45% of gasoline consumption, while biodiesel replaced 9% of fossil diesel, although legislation aims to reach 15% by 2023. Currently, most of the Brazilian light duty fleet is powered with flex-fuel engines, which are able to burn, with good performance, any blend from E100 to E27, hence explaining why ethanol participation is higher than the blending mandate. The remarkable reduction of ethanol consumption in the 2008-2012 period was essentially due to the elevated subsidies applied to gasoline in this period, moving consumers to fossil fuels.

FIGURE 4.3 Evolution of biofuel blending in gasoline and diesel in Brazil (% in volume)

FIGURE 4.4 Fossil fuels and biofuels consumption and biofuels participation in Brazil

a. Gasoline and ethanol

b. Diesel oil and biodiesel

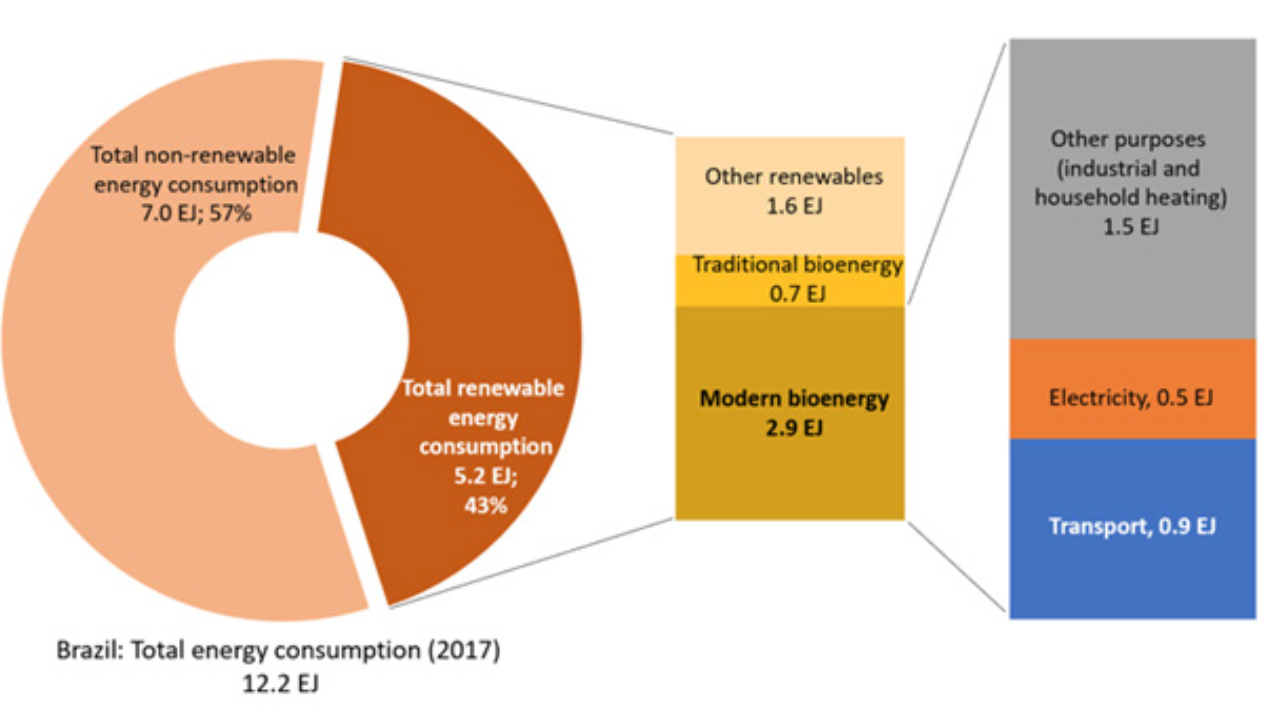

Modern liquid biofuels are part of the bioenergy production in Brazil, whereas biomass such as sugarcane bagasse, black liquor, and wood processing residues, are used as fuel for heat and power applications. In 2019, electricity from biomass reached 52.5 GWh, i.e. 8.2% of the total electricity generation in Brazil. Overall, bioenergy is the most important renewable energy source in the country (Figure 4.5).

FIGURE 4.5 Bioenergy in the Brazilian Energy Matrix

4.2.2 Biofuels Impacts and Land Use

As important as the energy contribution and emissions effects of biofuels, significant social and economic benefits can also be associated with their production and use. The sugarcane agroindustry alone, mostly adopting mechanized harvesting operations and modern cultivation practices, employs 870,000 workers and creates 2.5 million indirect jobs. It has been shown that sugarcane improves life conditions in regions where it is produced, as supported by a higher HDI compared to the neighboring regions. Furthermore, the accumulated savings of 3.15 billion barrels in gasoline imports avoided by ethanol production since 1975 was valued at 540 billion USD.

The modern bioenergy agroindustry, applying advanced technology and sustainability-oriented management in feedstock production and processing, allowed high yields and efficiencies, which resulted in a reduced land requirement. In Brazil, ethanol is produced mainly from sugarcane, complemented with corn, while biodiesel comes basically from soybean oil and tallow, with minor contributions from other vegetable oils. These feedstocks combined occupy about 11.2 Mha, i.e. 1.3% of national area. In fact, there is still a large room for promoting bioenergy on a sustainable basis, without affecting the production of other agricultural goods, neither harming natural forests nor biodiversity, especially through productivity gains and densification in livestock production.

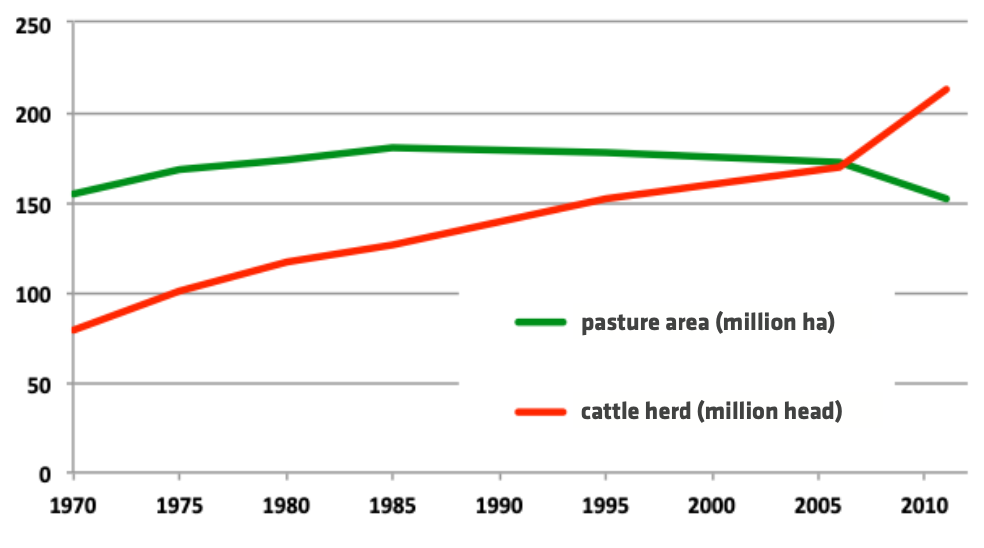

As indicated in Figure 4.6, cultivated and natural pastures occupy about 150 Mha in Brazil, 18% of the national territory, where the adoption of better practices has allowed an increase in production and freed land for other activities. Even marginal productivity gains in this large area can significantly expand the bioenergy supply. For instance, considering current best practices in Brazil, annual energy productivities of about 0.29 TJ/ha or 47 boe/ ha has been obtained.

FIGURE 4.6 Evolution of pasture area and cattle herd in Brazil

As a good indicator of the space for sustainable bioenergy expansion, in the Brazilian agroecological zoning for sugarcane, approximately 65.0 Mha are considered suitable for expansion, more than six times the current area. Among other restrictions, the following areas were excluded for this estimation: (a) land with slopes greater than 12% (unsuitable for mechanical harvesting), (b) areas with native vegetation, (c) Amazon and Pantanal biomes, (d) environmental protection areas, and (f) indigenous lands.

Therefore, the sustainable production of relevant volumes of biofuels can be well developed in areas of low productivity pastures with no need to use lands in the Amazon biome. It must be noted, however, that there is an urgency to promote (sustainable) economic activities in the Amazon, generating jobs and income distribution. In that sense, the production of oil palm in the currently degraded areas is an interesting option, as this can achieve high productivity while helping to recover the land. This means that the production of sustainable biofuels does not rely on the Amazon, but the desired development of the region may have biofuels as an important component. However, in order to be socially effective, governance and effective public policies (some already in place) must avoid undesired socioeconomic impacts, such as land grabbing, which may be one of the most delicate aspects for local communities and is not limited to biofuels initiatives.

4.2.3 The Essential Role of R&D

The remarkable evolution of efficiency and productivity of bioenergy production and use in Brazil was strongly supported by local R&D efforts, along the whole supply chain, from agriculture to final use, including process improvement, product diversification, and environmental impacts reduction. During the last decades, after initial studies and trials in Brazilian research centers and universities, a large set of new technologies were launched and progressively adopted. Some examples include the development of new plant varieties, biological control of pests, reduced tillage practices, precision agriculture, improved harvesting and transport, crop residue utilization, cogeneration, biogas production from stillage, and nutrients recycling, among several others. All of these efforts have led to less pollution and reduced consumption of chemicals and water, meaning reduced losses and more production, essentially by adopting more rational and environmentally responsible approaches, reinforcing the competitiveness of bioenergy production. With impressive results in ethanol agroindustry, after 30 years, energy productivity (in MJ/ha) increased by threefold and water consumption in the sugarcane mills was reduced to 5% of the original figures.

Additional relevant achievements can be expected in the forthcoming years, as indicated by the research results already available in Brazil. For example, new sugarcane varieties, selected and improved to yield more fiber and sugar, (also known as energy cane) have been introduced, doubling the conventional energy production per cultivated area. Also, second generation technologies are in pre-commercial operation. Several other innovations are under development, evolving the current agro-energy plants towards biorefineries, aligned with the broader concept of the modern bioeconomy. Particularly interesting for tackling climate change, assessments of CCS integration to ethanol mills are underway to make use of CO2 rich streams to enable negative GHG emissions from bioenergy, for example at ADM Illinois Industrial Carbon Capture and Storage (ICCS) project in Decatur, Illinois.

Complementing the R&D efforts and outcomes in biofuels production, their final use in road vehicles has also received attention In Brazil. Thus, new concepts have been introduced, such as electric turbocharging and flex fuel hybrid electric vehicles, increasing the efficiency of internal combustion engines; and fuel cell electric cars, fed with hydrogen produced on board by ethanol catalytic reform, which are currently in tests and demonstration on Brazilian roads. These improvements reinforce the advantage of biofuels.

4.2.4 Renovabio Program: An Environmental Breakthrough

Beyond the improvement of air quality in large cities, such as observed in São Paulo and Rio de Janeiro, the lower carbon footprint of biofuels allowed a significant reduction in GHG emissions in the Brazilian transport sector, representing an important contribution to the Brazilian NDC pledge in COP21. This positive effect has been acknowledged by the new Brazilian biofuels policy RenovaBio, launched in 2017. RenovaBio is a federal policy intended to reinforce the role of biofuels in the Brazilian energy matrix, in order to enhance energy security and mitigate GHG emissions, hence contributing to fulfill the Brazilian commitments under the Paris Agreement.

The program establishes annual decarbonization targets for the transport sector and includes sub-targets for fuel distributors. The objective is to create a market-driven mechanism to promote the expansion of biofuels in final energy demand, including land, sea, and air transport, based on sustainable practices and increased energy-environmental efficiency. The mechanism relies on a voluntary certification system through which biofuel producers can issue decarbonization credits (CBIOs) based on their respective carbon footprint. Financial institutions issue CBIOs which are freely negotiated at the stock exchange, and public policy will only be in charge of defining the long-term carbon reduction targets. Current decarbonization targets approved under RenovaBio will reduce the emission of 700 million tons of carbon from energy in the transport sector by 2029, making it one of the largest decarbonization programs in the world.

RenovaBio incorporates zero deforestation as one of the eligibility criteria for certification of biofuel producers. This means that biofuel production cannot be based on feedstocks coming from deforested areas, and all areas under cultivation must be registered under Brazil's strict Forestry Code's CAR (Rural Environmental Registry) requirements. More than a model of low carbon energy production, RenovaBio has consolidated a project of integrated economic development, using the potential for expansion of bioenergy production.

4.2.5 Final Remarks: A Vision of Future

Brazil offers a consistent example of the potential of biofuels, improved over decades in real large-scale systems, supplying competitive and low carbon fuels for a large vehicle fleet, with social and environmental advantages. Brazil has certainly succeeded in displacing fossil fuels by solar energy through biofuels, and in all scenarios forecasted for the forthcoming decades, this option is present.

This Brazilian experience has been successfully replicated in other countries as well; however, it can still be replicated/adapted in many other wet tropical countries, enabling a reduction of carbon emissions in the short term and increasing the sustainability of the energy sector as a whole. For this, land availability for expanding biomass production is more than enough and there is a large room for improvement in the production and use stages, assuring that it is possible and feasible to foster significant biofuel production and use in the short and long term. Indeed, biofuels can play an immediate and decisive role to decarbonize the transport sector, employing essentially the existing liquid fuel logistic infrastructure and the current vehicles fleet. However, although the Brazilian experience indicates that modern bioenergy can significantly reduce GHG emissions while promoting quality of life, it is unrealistic to expect that biofuels will solve all social and environmental problems alone. Complementary actions will certainly be necessary for the promotion of economic growth and in the pursuit of the Sustainable Development Goals.

4.3 The Case of the United States: Reimagining Biofuels as if Carbon Mattered

Lead Author: Tom Richard, Pennsylvania State University

4.3.1. The First Generation -- Biofuels as a Market for Agricultural Abundance and Energy Security

Historians remind us that the past is the prologue, so in mapping the future of bioenergy it is important to understand the historical context. Putting aside the thousands of years that bioenergy via fire was the primary human energy resource, and skipping over a few short forays into biofuels for transportation by Rudolf Diesel, Henry Ford and others, the modern biofuels industry really began to gather momentum in the US in the 1970s.

Although potential conflicts between food versus fuel dominate the debate about the role of biofuels in a sustainable future, it is important to note that the greatest challenge for the U.S. food system then, and arguably still today, was not scarcity but an overabundance of food. And today, as then, biofuels may offer a path toward sustainable development, but only if we learn from and address the challenges unveiled in the intervening decades.

In the mid 1970s the US beef industry started losing market share to poultry at an increasing rate, to the point that over a few decades per capita demand for beef dropped by over 30%.[6] Because poultry is much more efficient than beef at converting grains to meat, this dietary change led to a steep decline in demand for corn and soybeans. At the same time, biotechnology advances and improved crop management kept increasing grain yields year after year. Increasing supply and shrinking demand led to chronically low prices for farmers, while tight monetary prices caused farmland value to plummet.[7] During the farm crisis in the 1980s, farm bankruptcies were at levels not seen since the Dust Bowl of the 1920s and Great Depression of the 1930s. Low crop prices and economic stress were crushing rural communities and driving young people away from farming. The U.S. also had its first "peak oil" in 1970, and in subsequent decades experienced declining domestic oil production, increasing imports, and frequent price shocks.[8] In this context corn ethanol and soybean biodiesel gained widespread political support and strong financial subsidies to address concerns of energy security, farm income, and rural economic development.[9]

The environmental attributes of biofuels were always recognized, but in a secondary role, with the first real environmental driver being the use of ethanol as an oxygenate in gasoline to improve combustion, replacing the carcinogenic petroleum-derived methyl tert-butyl ether (MTBE) that had contaminated groundwater through spills and leaking underground storage tanks.[10] That substitution resulted in a new standard that gasoline vehicles be designed for blends of up to 10% ethanol. That 10% ethanol content became a defacto "blend wall", slowing growth in demand soon after ethanol production reached 10 billion gallons per year in 2009. While subsequent testing by manufacturers and the US Environmental Protection Agency (EPA) now allows vehicles built since 2001 to use blends up to 15% ethanol, that cap has effectively constrained demand to about 15 billion gallons per year since 2015 (see figure 4.3.1).[11]

4.3.2 A Lost Decade: Cellulosic Biofuels Boom and Bust

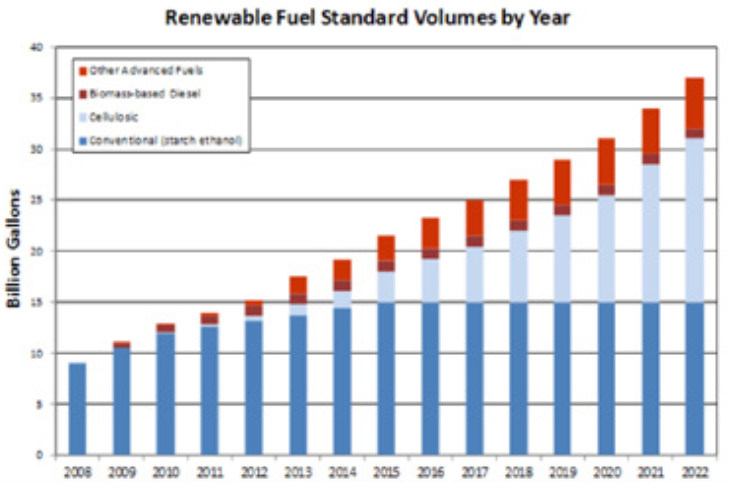

The biofuels industry entered the first decade of the new millennium with both political and economic momentum. Climate change was gaining widespread attention, and cellulosic biofuels were recognized for their potential to reduce greenhouse gas emissions. Both private industry and federal agencies projected that the cellulosic biofuel industry was technically ready for commercialization. There was widespread belief that the primary limitation to commercialization was financing, which could be solved by guaranteed markets. Soon the U.S. Congress was ready to expand support for biofuels, passing the Energy Independence and Security Act of 2007.[12] These revisions to the Renewable Fuel Standard (RFS2) set annual fuel volume requirements that blenders and distributors of petroleum fuels had to meet, resulting in an EPA regulated market for renewable fuels and their associated Renewable Identification Numbers (RINs) by petroleum fuel distributors. Volume requirements were set for different categories of biofuels, with volumes for first generation biofuels of starch ethanol and biodiesel only expanded slightly. Of the nearly 400% growth projected for the 15 years ending in 2022, almost all would be in the categories of cellulosic and other advanced biofuels that have a greatly reduced carbon footprint relative to fossil fuels. Separate volume requirements were set for each fuel category, and thus guaranteed markets with higher prices were expected to subsidize the rapid growth of the most low carbon cellulosic and advanced biofuels.[13]

FIGURE 4.3.1. The U.S. Energy Independence and Security Act of 2007 legislated annual renewable fuel volume requirements for defined categories of biofuel.

Shortly after the 2007 legislation became law, several companies announced plans to build cellulosic biofuel plants, and within a few years three were fully built in the U.S. and several others started. But then came the bust, and as with the boom there were a constellation of factors involved. First, the technology was simply not ready. Processes that worked in the laboratory or small pilot facilities faced challenges at commercial scale.

These challenges were exacerbated by the rush to build full-scale commercial plants that were often thousands of times larger than any proven pilot scale, despite prudent industry practice indicating that scale-up with solid feedstocks should step up by a factor of ten to twenty at most. Biomass logistics were also an issue, ranging from challenges with negotiating farmer contracts to major fires in storage depots. Not one of that first round of second generation cellulosic biofuel biorefineries is regularly operating today.[14]

Beginning in 2008 and continuing to the present, overcoming these commercialization challenges has been hindered by a softening of public and private support. Public support for biofuels was first challenged by perception that food production is in conflict with biofuels. This concern coincided with rapid growth of the starch ethanol industry in the 2000's, so that by 2008 roughly 40% of the U.S. corn crop was used for that single purpose. That year prices for corn and other grains spiked, and biofuels were blamed for grain scarcity and higher food prices, igniting a "food versus fuel" debate. While those price spikes and grain shortages were eventually found to be largely due to other factors including crop failures due to drought elsewhere in the world, the public mindset was fixed.[15] That concern about food production was reinforced by several scientific papers in 2008 and subsequent years projecting that biofuel demand induced land use change and conversion of native ecosystems including tropical rainforests that greatly diminished and might even overcome any greenhouse gas emission benefits of biofuels relative to fossil energy.[16] Although later studies dramatically reduced those early estimates, the views of many environmental groups and much of the public had shifted to a negative view of biofuels.[17]

A second factor in reducing public support was the rapid increase in domestic oil and gas production due to hydraulic fracturing. U.S. production of natural gas began growing rapidly in 2005 and the shale oil boom followed in 2008, growing so rapidly that the previous 1972 peak in domestic oil production was surpassed in 2018 and is even higher today. The oil and gas industry became less concerned about shortages and more concerned about growing markets for fossil oil and gas. While some U.S. auto manufacturers were prepared to shift to make internal combustion engines to be more compatible with ethanol (the easiest and most efficient liquid fuel produced from biomass, including from cellulose), there was a growing call from the petroleum industry, the aviation industry (see next section) and others for "drop-in" fuels that were 100% compatible with existing engines and infrastructure, often implying that was the only way to overcome the "blend wall".[18] Not surprisingly, these drop-in fuels have proven much more difficult and more expensive to make than ethanol. In the last decade, government and academic researchers have spent over a billion dollars on research on drop-in fuels, and the only large-scale commercial successes thus far have been based on either first generation vegetable oil feedstocks or, for cellulosic feedstocks, the gasification and Fisher-Tropsch technology developed in World War II and expanded in South Africa to make liquid fuels from coal in response to sanctions during the apartheid era.[19] With limited public and political support and continuing technology challenges, renewable energy investment capital shifted to less controversial renewables like solar and wind.[20] This flight of investment capital continues to limit growth in the U.S. biofuels industry with two important exceptions -- aviation fuels and renewable natural gas.

4.3.4 Aviation Biofuels

Although the commercial success of electric vehicles is a more recent phenomena than the call for drop-in fuels, they have been mutually reinforcing. With the rapid advances in batteries and electric vehicle technologies, new questions have been raised about whether there is even a need for transportation biofuels in the future. Long term projections by the U.S. Department of Energy, the International Energy Agency, and others indicate that heavy duty transportation and specifically commercial aviation will be most reliant on liquid fuels. Finding substitutes for commercial aviation is particularly challenging for several reasons: from a technical standpoint liquid fuels have a far higher energy density than batteries or even gaseous fuels on a volumetric basis, so for long distance flight fuel storage space is a major constraint; each airplane can remain in commercial service for many decades, so every airport will need to service the existing fleet with liquid fuels well past 2050 greenhouse gas reduction targets; and jet engines are already very efficient, so there is little potential to double mileage efficiency like the automobile industry is on track to achieve.[21]

For all these reasons the commercial aviation industry has encouraged and welcomed the pivot in U.S. government research and demonstration funding to "drop-in" fuels. While many airlines are purchasing small volumes of aviation biofuels today, most current commercial processes use vegetable oil as feedstock, which has a similar cost to conventional jet fuel and limited per acre yield. There are commercial aviation biofuel alternatives based on sugars and starch (with similar food versus fuel constraints) or thermochemical technologies such as gasification and Fischer-Tropsch catalysis. Many other drop-in fuel technologies have been proposed and even demonstrated at laboratory scale, but commercial scale-up remains in its infancy.[22]

4.3.5 The Rise of Renewable Natural Gas -- The Surprise Drop-In Fuel

While the legacy of the 1970s oil crisis lingers on in the policy support for liquid biofuels for transportation, in the last five years it is a gaseous biofuel that has experienced the most rapid growth. Renewable Natural Gas (RNG), or biomethane, is chemically identical to the methane molecule that comprises over 95% of fossil natural gas. While the U.S. Renewable Fuel Standard (RFS) categories of cellulosic biofuels and advanced biofuels were written with liquid fuels in mind, in 2014 the EPA made a determination to expand the cellulosic biofuel category to include the methane from landfills and anaerobic digestion, categorizing landfill waste and on-farm agricultural feedstocks as cellulosic by definition, and therefore eligible for the most lucrative subsidies in that program.[23] The state of California provides an even larger subsidy for many types of RNG through their transportation- focused Low Carbon Fuel Standard (LCFS).[24] Suddenly landfills and farms that had been converting biogas (a mixture of roughly 60% methane and 40% CO2) to electricity found that these transportation subsidies were much more lucrative than renewable electricity, and since 2014 over 95% of the cellulosic biofuel sold in the U.S. has been RNG.[25] Both the RFS and LCSF markets are constrained by there being enough natural gas vehicles buying RNG for transportation to justify all the RNG subsidies, but thus far that usage has exceeded the supply. With shale gas continuing to be low cost and abundant, many public and commercial transportation fleets have been converting vehicles to natural gas, staying ahead of the surge in investment in RNG projects at landfills and farms.

While the initial growth of RNG in the U.S. has primarily been driven by subsidies for transportation biofuels, most fossil natural gas is used for electricity and process heat. As these sectors also shift to renewable sources, new markets for RNG are expected to expand, with the natural gas grid providing very low cost distribution to a massive customer base. Already some businesses and governments are contracting for RNG to replace their fossil natural gas in heat and power applications, allowing significant reductions in the corporate greenhouse gas footprint. As intermittent renewables like solar and wind supply even larger fractions of the electricity portfolio, RNG fueled gas turbine generators will compete with grid-scale batteries to provide easily stored and dispatchable electricity. Although the term "drop-in" fuel was originally intended to describe liquid biofuels for transportation, RNG can compete favorably not just for transportation but also heat, electricity, and manufacturing. With fossil natural gas now the dominant energy source across all these sectors in the U.S., meeting future goals to reduce GHG emissions may require a larger role for RNG, perhaps the ultimate drop-in fuel.

4.3.6 CO2 Storage Arrives

RNG is not the only opportunity for bioenergy to leverage U.S. fossil energy investments. Over several decades the U.S. Department of Energy (DOE) has invested billions of dollars developing technologies for the capture and geologic storage of CO2 from coal-fired power plants. The U.S. has suitable geology to store over a thousand years of CO2 at current emission rates. Carbon capture from flue gas at power plants has proven technologically complex and expensive to scale-up. But most biofuel conversion processes produce concentrated CO2, either as a byproduct of ethanol fermentation, the residual gas after RNG purification from biogas, or as a byproduct of syngas cleanup in a thermochemical biorefinery.[26]

For these reasons, a corn ethanol biorefinery owned by ADM is now the first U.S. commercial source of CO2 to be stored underground, funded initially as a DOE demonstration project and currently injecting a million Mg of CO2 annually. That facility overlays appropriate geology so there are no transport costs, but for more dispersed networks the costs of pipeline transport of CO2, plus injection and monitoring of a geologic storage site, are estimated at between $30 and $60 per Mg of CO2.[27] Federal tax incentives passed in 2017 cover most or all of those costs, and any geologic CO2 storage associated with biofuels sold in California for transportation can earn additional incentives of nearly $200 per Mg of CO2 through the Low Carbon Fuel Standard marketplace. As a result of these incentives and synergies, biofuel facilities are poised to dominate the near-term growth of CO2 storage in the U.S. In early 2021, Summit Carbon Solutions announced a $2 billion pipeline that will gather CO2 from corn ethanol facilities in several Midwestern states for geologic storage.[28]

With the right feedstocks and processing strategies, Biomass Energy Carbon Capture and Storage (BECCS) can not only reduce emissions, but actually produce net carbon negative energy. Relative to regular biomass energy systems, adding BECCS can capture an additional 33% of the biomass feedstock carbon in an ethanol fermentation, 40% in anaerobic digestion when separating biogas to RNG, 50% from thermochemical fuel catalysis, and over 95% from a bioelectricity plant.[29] BECCS has been widely viewed by the Intergovernmental Panel on Climate Change and others as the primary strategy for offsetting fossil emissions by mid-century, and is projected to be drawing down atmospheric CO2 concentrations at a gigaton scale by 2100.[30] But achieving those goals will require substantial investment in research, development, and deployment, as maximizing the climate mitigation potential of bioenergy requires advances in both sustainable feedstock production and conversion technology.[31]

4.3.7 Sustainable Feedstocks: Realizing the Potential of Carbon Negative Biofuels

At the scale of the earth system, photosynthesis captures ten times as much CO2 as is emitted by current fossil energy production. Some of that carbon captured by photosynthesis is stored in forests, soils, and other ecosystems, and net ecosystem carbon storage at a large scale can provide a substantial "natural solution" to climate change.[32] But in most ecosystems, nearly all of that captured carbon quickly returns the atmosphere through decomposition or fire. Unfortunately, many human interventions including land clearing, cultivation and drainage associated with conventional agriculture can lead to net ecosystem carbon loss. To get to a meaningful carbon negative system, termed "additionality", requires (1) increasing photosynthetic carbon uptake and/or (2) reducing losses that normally return to the atmosphere via respiration or combustion. Recognizing that the fundamental problem of U.S. agriculture is currently abundance, not scarcity, and that the need for negative emissions is already massive and needs to grow, it is important to consider the sustainability of biomass feedstock alternatives with respect to their climate mitigation potential, their impact on ecosystem services, and potential synergies with food production systems. There are many win-win options for food and biofuel.

Increasing photosynthetic carbon capture (additionality #1) can be accomplished in several ways. In the U.S., plant breeding programs have been successful in increasing biomass yields and thus carbon capture for a range of bioenergy crops. These include first generation biofuel crops like corn, soy, and canola; cellulosic annual crops such as biomass sorghum; perennial grasses such as switchgrass, miscanthus, and energy cane; and short rotation woody crops including willow and poplar.[33] Other ways to increase photosynthesis include various strategies of sustainable intensification: planting bioenergy double crops like winter rye, which could provide over 100 million Mg yr-1 of biomass feedstock on existing cropland during times of the year the land is normally fallow;[34] precision management of water and fertilizers to optimize yields while minimizing N2O emissions or losses to surface and groundwater; and planting robust, high yielding perennial biomass crops on marginal field or subfield areas where less resilient annual crops grow poorly some years due to flooding, drought, insects, disease or other stressors.

Recent studies have found that 20% or more of U.S. cropland is economically marginal for annual food crop production.[35] Much of that land can be converted to bioenergy crops with minimal impacts of food production, and with significant improvements in ecosystem services ranging from soil carbon to biodiversity to water quality.

Other sections of this report have emphasized the "no regrets" advantage of waste materials as bioenergy feedstocks. These organic materials include food waste, wood waste, industrial sludges from food and other bioprocessing industries, as well as farm manure and crop residues. If there are any negative impacts on the environment during their production, those impacts and any associated land use change will be debited against the primary product and not the waste. If not used for bioenergy these potential feedstocks would otherwise be decomposing, with their carbon being released to the atmosphere though microbial respiration. For these feedstocks, additionality #2 can be realized in several ways. Biomass systems that divert that decomposing carbon to fuels or other energy products can earn an offset against the fossil emissions they displace. If the residues from fermentation, pyrolysis (biochar) or other processes are returned to the land some or most of that carbon can be sequestered in the soil, potentially longer and to a greater extent than if the original wastes were left on the soil surface or disposed in a landfill. BECCS is an extreme form of additionality #2, and couples well with cellulosic bioenergy crops (additionality option #1).

It is important to recognize that with current technology options, not all locations are appropriate for advanced cellulosic biofuel systems. For example, feedstock production is unlikely to be sustainable on sites or with crops that require irrigation, as the energy and environmental costs of pumping water and the depletion of surface and groundwater aquifers could exceed any carbon mitigation benefits from biofuels. With current technology, it is also difficult to justify converting healthy forests to biofuel production. In the forested landscapes of the Eastern U.S., the carbon mitigation potential of current cellulosic biofuels technologies without BECCS is roughly equivalent to carbon storage in the equivalent natural ecosystem, so there is no benefit to investment. In the temperate rainforests of the northwestern U.S., natural ecosystems can accumulate carbon for centuries before their high rates of carbon mitigation slow. In contrast, because of the much lower amount of carbon stored in a grassland ecosystem, implementing the same current cellulosic biofuel technologies could mitigate carbon emissions by 3X (300%) on a per hectare basis.[36]

Cellulosic biofuel production on marginal cropland and grassland has tremendous carbon mitigation potential, and that potential increases with higher crop yields (additionality #1), more efficient conversion technologies, and BECCS (additionality #2). But additional research, development, policy, and financial support are needed to realize that potential. Such support is needed to identify appropriate feedstock types and locations, develop and implement advanced cellulosic biofuel technologies, and create the pipeline and subsurface infrastructure needed for BECCS. With such investment, biofuels and BECCS can be a strong driver for increasing the sustainability of agricultural systems and reversing climate change through negative emissions. Relative to natural ecosystems in the eastern U.S., advanced biofuel systems using perennial grasses as feedstocks and incorporating BECCS for the byproduct CO2 streams could provide between 5X (forest ecosystems) and 14X (grassland ecosystems) greater carbon mitigation benefits.[37] Integration of biofuels with food crops can also generate important synergies. The BiogasDoneRight approach, pioneered in Italy, uses anaerobic digestion to convert winter crops, crop residues, livestock manure, and agro-industrial wastes to biogas, which can then be used to produce either electricity or RNG. This approach is currently being piloted on farms in the U.S., and if fully implemented, could generate sufficient RNG to replace roughly 10% of current fossil natural gas supplies while also enhancing soil and water quality, improving nutrient cycling, and increasing food production.[38]

Perhaps the most important lesson from the U.S. experience is that there are both good and bad ways to implement biofuels. Winter bioenergy crops and perennial grasses can play a critical role in increasing biodiversity and improving soil health, forming a foundation for regenerative agriculture with benefits to ecosystem services, rural economies, and also with strong carbon mitigation. But there are also ways to implement biofuels poorly.

Corn production, which is the dominant biofuel feedstock in the US today, can result in degraded ecosystems, eroded soils, and contaminated waterways. Policies are needed to guide project development toward the better alternatives. These policies need to be based on sound science, and backed by quantitative tools, such as life cycle analysis, to assess the many dimensions of sustainability. Performance based incentives, such as California's Low Carbon Fuel Standard, have proven effective at stimulating innovation and accelerating deployment of biofuels with a low carbon intensity. Similar incentives that reward other indicators of social and environmental sustainability, and drive biofuels from "low carbon" to "negative carbon", are also needed. In 2011 the Nuffield Council on Bioethics proposed an International Ethical Standard for Biofuels that addressed human rights, environmental sustainability, climate mitigation, fair trade, justice, and equity.[39] Because of the recognized potential of biofuels to address climate change, the last principle stated that if the other ethical criteria were met, there is an ethical responsibility to develop biofuels. Now a decade later, with global CO2 levels continuing to climb, the imperative to develop and scale-up sustainable, carbon negative bioenergy systems is greater than ever before.

4.4 The Case of the European Union: The Untapped Potential of Wastes and Residues for Sustainable Biofuel Production

Lead Author: Emanuele Oddo, Politecnico di Milano

EU countries made a great effort in recent years to define more ambitious targets for sustainability in order to stay on track for the 2050 goals. Many countries are close to the 10% target for renewable share in transport for 2020 and some countries are even above. The same is true also for the overall share of renewable sources.

Although some countries still fall short, the EU is currently the largest producer of biodiesel worldwide and among the top producers of advanced biodiesel/HVO with the US.

The deployment of advanced platforms for biofuel production is undoubtedly tied to the strong commitment of EU policies. Indeed, IEA reported that if long-term targets for novel advanced biofuels are met, they will prompt investment in new technologies and encourage biofuel feedstock diversification so that the EU will get halfway to its 2025 interim target.[40] Furthermore, one of the greatest benefits coming from the efficient conversion of wastes/residues for biofuel is in terms of land and water impact. Wastes need to be disposed of one way or the other -- and owners are often willing to pay to get rid of them -- and they usually do not imply land usage or water consumption to be fed to the process, thus lowering significantly the impact related to biofuel production.

4.4.1 The framework of EU renewable energy policies

The EU introduced over the years many policies to foster the sustainable evolution of EU countries towards climate neutrality for 2050. Such initiatives collectively fall under the frame of the European Green Deal, which is articulated in macro-areas of intervention, including sustainable mobility. In this respect, a substantial measure to foster biofuel production is surely the Renewable Energy Directive (RED II) of 2018. The directive implies demanding goals for the coming years:

35% improvement in energy efficiency;

32% share of renewable in energy consumption within EU by 2030;

14% share of biofuels in transport fuel consumption by 2030;

Less than 7% food crops as feedstock for biofuel production.

The directive will have to be transposed by member states by June 2021. The 32% target of renewable energy will be achieved by EU countries collectively. As for the transport sector, fuel suppliers in each Member State are required to incorporate at least 14% of renewable energy by 2030, following the indicative guidance set by national authority. Moreover, biofuels based on feedstocks which are not meeting sustainability criteria (e.g. 1G feedstocks with food-vs-fuel or water footprint issues) are expected to be progressively phased out starting from 2023. The Renewable Energy Directive also addresses advanced biofuels and biomethane from municipal solid waste (MSW) and agri-food residues with a sub-target of 3.5% by 2030.

In addition, Annex IX-A and IX-B reports two lists of advanced feedstocks for biofuel production, namely algae, MSW, agri-food and forestry residues and municipal or industrial waste for Part A and used cooking oil (UCO) and animal fats for Part B. This is particularly relevant considering that the double count mechanism is applied to Annex IX biofuels. This means that biofuel obtained entirely from waste and residues are double counted for the purpose of determining renewable energy units (HEB). This is clearly one way to incentive the production of advanced biofuels among the Member States, even though Annex IX-B feedstocks are capped to 1.7% for the 2030 target (but Member States may request higher limits for proven feedstock availability). Moreover, these communitarian initiatives still need to be implemented by each EU country and may undergo some modifications. This is all the more true considering that the European Commission has planned a revision of the RED II by the end of 2021, to foster the EU's increased climate ambition.[41]

In addition to RED II, a set of other directives also foster waste and residues mobilization by preventing or discouraging landfill disposal. This includes the Waste Framework Directive 2008/98/EC and the Industrial Emission Directive 2010/75/EC for air and water protection, which limits landfill disposal of waste organic fraction to both encourage re-use and prevent possible threats to public health. Broadening the view, all these actions are shaped within the general framework of the European Green Deal, which aims to cut 90% of GHG emissions within the transport sector by 2050.

4.4.2 Cutting edge biofuel production in Nordic countries

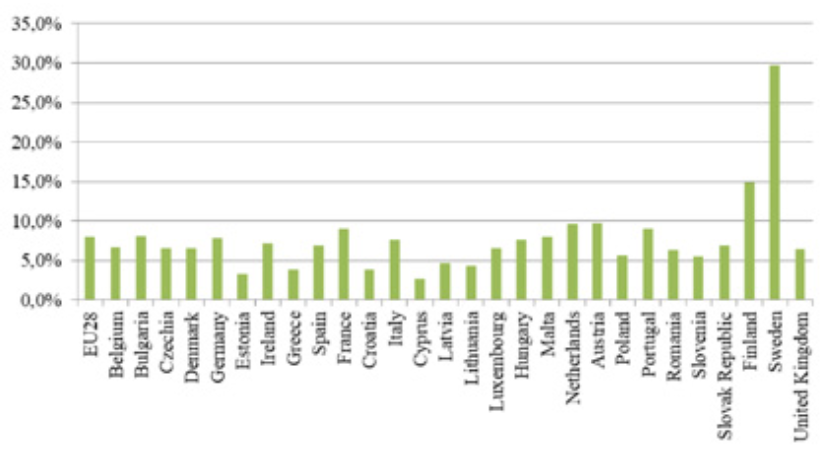

Northern Europe countries are the forefront of advanced biofuel technology and biofuel production in general. Indeed, the biofuel share in the transport sector for Nordic countries is very high compared to the other member states (see Figure 4.4.1), with Finland surpassing the average by at least 5% and Sweden almost reaching 30% in 2018. Such a gap is still evident for 2019 figures, where Finland energy share in transport climbed to 21.3%, compared to an EU average of roughly 9%, while Sweden raised its own share to 30.3%, retaining the highest share in the EU by a wide margin.[42] These huge achievements are also the result of very ambitious policies within Nordic countries, giving rise to a wide array of ventures for advanced biofuel production.

FIGURE 4.4.1. Share of renewable energy in the transport sector per EU Member State in 2018.[43]

In Finland, Neste is surely the leading group for sustainable fuel production with an ensemble of five refinery lines divided between Porvoo and Naantali. Although the main products in the Porvoo complex come from crude refining, the facility is also equipped with NEXBTL units, providing renewable diesel through hydrotreating of waste oils and fats. These production lines yield drop-in biofuel viable for either road or marine transport as well as renewable naphtha and propane, providing higher flexibility to the plant.[44] The renewable diesel coming entirely from waste -- known as Neste MY Renewable Diesel -- was launched in 2017 at Helsinki in many service stations.[45]

UPM is also operating a biorefinery in Lappeenranta, Finland. Opened in 2015 with a 179 million euros investment, the plant is converting wood residues, mainly pulp tall oil and paper mill wastes, to HVO. It is located next to a paper mill facility to ease the supply of raw materials and it provides 130,000 tons per year of biodiesel. Additionally, the plant opening guaranteed 250 new employees through direct or indirect work positions.[46] The company is also considering the opening of another plant in Kotka with a capacity of about 500 million liters, for the conversion of forest residues, like sawdust and branches, to biofuels for road and marine sectors.[47] Another company exploiting pulp residues is Södra, which began production of biomethanol in Mönsterås, Sweden. The plant is based at the pulp mill and it has a capacity of roughly 6 million liters per year.[48] The biomethanol can be used either as a transport fuel or as platform chemical (e.g. for the production of diesel). The feasibility of this route is certainly strengthened by the great versatility of methanol, which is a common brick of the organic chemistry industry, providing many industrial applications.

Another relevant production in Sweden is surely the Preem plant in Gothenburg, producing 160 million liters of HVO from tall oil. The company is also planning to expand the capacity to 1.3 billion liters in 2023. Both Preem and St1 are planning to start the production of bio-jet fuel in Gothenburg in 2022, with production capacities of 250-300 million liters. The main feedstocks will again be either UCO and waste fats, as expected considering the double counting incentive. Pyrocell, which is owned by Preem, is considering a production line for the conversion of wood residues into pyrolysis oil.[49] The plant will be located in Gävle, Sweden, and should process up to 40,000 tons of dry feedstock. Green Fuel Nordic Oy has also established a partnership with the Dutch BTG for the opening of a pyrolysis oil plant using sawmill by-products in Lieksa, Finland.[50] Finally, St1 Biofuels Oy launched a cellulosic ethanol plant with a 10 million liters capacity in 2018 and it is planning to build three 50 million liters plants in Kajaani, Pietarsaari and Follum (Norway).[51]

This large ensemble of production lines is also possible thanks to the cutting edge policies implemented in Nordic countries. In fact, Finland has established a 30% target of biofuels in transport by 2030, paired with a 10% target for advanced biofuels in the same sector. In Sweden, liquid biofuels are exempted from energy and CO2 taxation, to increase their use in the transport sector, and the European Commission has approved the prolongation of such tax exemption to 31 December, 2021.[52] Despite being the leading country for biofuel share and already well above the 10% target for 2020, Sweden has also committed the reduction of GHG reduction in the transport sector by 70% compared to 2010 level by 2030. Even though this measure does not account for the aviation segment, it is still a challenging objective. Production of HVO/HEFA is very relevant in these countries, also due to the double-counting system, which was accepted by both Finland and Sweden.

4.4.3 The potential of hydrotreating platform for transport

More in general, production of hydrotreated biofuels is a relevant asset for the entire EU panorama. This is due to many reasons, the first being the double-counting system. This system is implemented in many EU countries, allowing double-count biofuels produced entirely from waste and residues. Moreover, hydrotreating allows easy repurposing of existing infrastructure and it is currently the only viable way to ensure bio-jet to feed the aviation segment. As a result, many companies are operating or planning to construct/reconvert plants into full HVO production.

For instance, Total has launched in 2019 the La Mède plant in France, producing 500,000 tons each year of HVO biodiesel. The biofuel is obtained from 60-70% of vegetable oils and 30-40% of wastes, including UCO and animal fats. Total has pledged to keep palm oil consumption below 300,000 tons per year and to incorporate at least 50,000 tons of French-grown rapeseed into the raw materials. This would create the opportunity for a new domestic market.[53]

Apart from the aforementioned plants in Finland, Neste has also launched two other plants in Singapore (2010) and Rotterdam (2011), for the exclusive production of renewable products, with capacities respectively of 1.3 and 1 million tons per year.[54][55] At the end of 2018, Neste has announced a 1.3 billion euros investment to raise the Singapore refinery capacity up to 4.5 million tons per year.[56] This intervention fits in the Neste plan to raise its renewable jet-fuel capacity from about 120 million liters to 1.2 billion liters, whose main production will be located in Singapore. The main feedstocks are again waste fats and oils, covering 80% of the feed in 2018, and Neste has pledged to reach 100% waste and residues by 2025.[57]

ENI has also strongly invested into conversion of waste to renewable diesel and jet-fuel. A former crude oil refinery in Venice was reconverted to biorefinery in 2014 in the framework of the "Green Refinery'' project. Since then it has been processing 360,000 tons per year of pre-treated vegetable oils, UCO and animal fats to renewable diesel according to the proprietary technology Ecofining™. Recently, a 500 million euros investment was made to allow direct processing of crude vegetable oils, raising the processing capacity to 560,000 tons per year and the output to 420,000 tons per year.[58] Thanks to several agreements with national consortia, Porto Marghera biorefinery is currently processing 50% of all the UCO available in Italy.[59] The Venice experience is a clear example showing that repurposing of existing infrastructure is possible for hydrotreating with relatively moderate investment costs. This will clearly reduce the risk connected to the deployment of the technology, fostering its deployment.

Another plant has been launched in 2019 in Gela, with a processing capacity of 750,000 tons per year. Again, the biorefinery comes from the repurposing of existing infrastructure with a 360 million euros investment. The plant can be fed interchangeably with many advanced 2G/3G feedstocks, including UCO, tallow and algae.[60] Given the high flexibility of such plants, ENI has pledged to totally replace palm oil with advanced feedstocks by 2023. This is a huge effort, implying mobilization of roughly 1 million ton per year of alternative raw materials.

The Gela facility also hosts a Waste-to-Fuel pilot plant, converting organic fraction of MSW into 250 tons per year of bio-oil, the result of a 3 million euros investment. This is relevant considering that hydrothermal liquefaction is generally a neglected route for biofuel production, although it provides great advantages compared to other thermochemical processes (milder conditions, one-phase output, sound efficiency). Looking at the whole country, Italy produces about 30 million tons of waste per year. 14 million tons are correctly separated and about 7 million tons make up the organic fraction. By improving waste collection, separation and management, the available organic fraction could be raised up to 10 million tons. Should this reservoir be devoted to bio-oil conversion, it would yield a billion liters per year of bio-oil, which corresponds to about 6 million barrels of crude oil per year.[61] This would be paired with a considerable production of water - it makes up roughly 80% of the process output - which could be employed for industrial purposes, possibly in integration with other processes.

As a final remark, given the available infrastructures, the two major constraints of the hydrotreating platform are essentially raw material costs and hydrogen supply. The former is typically overcome when dealing with 2G waste feedstocks. As for the latter, it has been proposed to implement the local production of green hydrogen (i.e. from electrolyzers) to directly supply the hydrotreater. The process would clearly benefit from this in terms of carbon balance, especially if the electrolyzers can be powered through bio-energy. In fact, ENI is planning in collaboration with ENEL the realization of two 10 MW pilot plants to produce green hydrogen, which could be exploited in place of conventional H2 from steam reforming. The company is also investing to expand its facility near Ravenna, which is currently devoted to CCS and blue hydrogen, which may again be exploited to supply H2 for hydrotreating.

4.4.5 Perspectives on the potential of wastes

The previous examples clearly highlight that there is a high potential connected to the mobilization and conversion of waste and residues. The economic profitability of such processes is evident, considering that many companies are currently investing to expand their businesses in this field. Moreover, the EU and national policies for stimulating waste-based biofuels have been effective in significantly raising the biofuel share. This is especially true in Nordic countries, where national policies are not just in compliance with the EU frame, but they are even more demanding. Although the EU is still the leading continent in such a field, a large room for improvement is available. Indeed, only a minor share of the huge reservoir of wastes have been exploited.

It was estimated that about 44 million tons of MSW will be available for biofuel production in the EU in 2030.[62] The organic fraction of such wastes is partially devoted to recycling or incineration, but the remaining is typically disposed of in landfills, where the decomposition to methane may have adverse climate effects if left unchecked.

As for crops residues, the production varies widely between EU countries, due to the wide differences in farming techniques, and some of these feedstocks are already exploited for other uses. However, about 122 million tons are considered to be sustainably available now and 139 million tons are expected to be disposable in 2030.[63] Forestry residues are not trivial to be mobilized for several reasons, including soil balance and low bulk density. Still, 80 million tons of forestry residues are produced each year in the EU, yielding 40 million tons sustainably available for harvesting without causing soil depletion.

Finally, more than 1.1 million tons of used cooking oil was consumed in 2013 in the EU, with substantial imports.[64] Thus, an increase in the collection efficiency of used cooking oil within the EU would be desirable to satisfy such demand. This could come from household collection, although it would imply a relevant effort in terms of behavior change, and from oil separation in wastewater treatment plants. Certifications may also play a key role in asserting a common degree of quality of processed oil and resulting biofuels.

UCO import in the EU is not the only issue related to trade. Indeed, waste displacement between EU countries is also relevant, due to the different capacities in waste management among the countries. This results in rather different gate fees for waste management and treatment, making waste processing far more convenient in some countries compared to the others (for instance, the UK may be willing to take advantage of more convenient gate fees in Germany or in the Netherlands[65]). More generally, a great disparity is still found among countries in terms of policies enactment and harmonization with the EU framework, which is probably one of the strongest barriers preventing advanced biofuel deployment throughout the continent.

Goh, C. S. & Lee, K. T. 2010. Will biofuel projects in Southeast Asia become white elephants? Energy Policy, 38, 3847-3848. ↩︎

Jaung, W., Wiraguna, E., Okarda, B., Artati, Y., Goh, C., Syahru, R., Leksono, B., Prasetyo, L., Lee, S. & Baral, H. 2018. Spatial Assessment of Degraded Lands for Biofuel Production in Indonesia. Sustainability, 10. ↩︎

Ahmed Et Al., Using The Ecosystem Service Approach.; Goh, C. S., Wicke, B., Potter, L., Faaij, A., Zoomers, A. & Junginger, M. 2017. Exploring Under-utilised Low Carbon Land Resources From Multiple Perspectives: Case Studies On Regencies In Kalimantan. Land Use Policy, 60, 150-168. ↩︎

Smit, H. H., Meijaard, E., Van Der Laan, C., Mantel, S., Budiman, A. & Verweij, P. 2013. Breaking the Link between Environmental Degradation and Oil Palm Expansion: A Method for Enabling Sustainable Oil Palm Expansion. PLoS ONE, 8. ↩︎

Gibbs & Salmon, Mapping The World's Degraded Lands. ↩︎

"Agricultural Economic Insights | Pass The Meat: U.S. Meat Consumption Turns Higher". 2021. Agricultural Economic Insights. [https://aei.ag/2016/10/31/u-s-] [meat-consumption-turns-higher/]. ↩︎

Barnett, B.J. 2000. The U.S. farm financial crisis of the 1980s. Agricultural History 74(2):366-380 ↩︎

Bardi, U. 2019. Peak oil, 20 years later: Failed prediction or useful insight? Energy Research & Social Science 48:257-261. ↩︎

Tyner, W.E. 2008. The US Ethanol and biofuels boom: its origins, current status and future prospects. BioScience 58(7):646-653. [https://doi.org/10.1641/] [B580718]. ↩︎

Connor J.A., R. Kamath, K.L. Walker, and T.E. McHugh. 2015. Review of quantitative surveys of the length and stability of MTBE, TBA, and benzene plumes in groundwater at UST sites. Ground Water 53(2):195-206. doi: 10.1111/gwat.12233. ↩︎

- ↩︎

"H.R.6 - 110Th Congress (2007-2008): Energy Independence And Security Act Of 2007". 2021. Congress.Gov. [https://www.congress.gov/bill/110th-congress/] [house-bill/6]. ↩︎

U. S. Environmental Protection Agency, Assessment and Standards Division, Office of Transportation and Air Quality. 2010. Renewable fuel standard program (RFS2) regulatory impact analysis. United States Environmental Protection Agency, Washington, DC. [https://nepis.epa.gov/Exe/ZyPURL.cgi?Dockey=P1006DXP.TXT] ↩︎

"Next-Gen Biofuel Dreams Fade; Developers Blame EPA". 2021. Agri-Pulse.Com. [https://www.agri-pulse.com/articles/12894-cellulosic-ethanol-struggles-to-] [climb-commercialization-ladde]r. ↩︎

Zhang, Z., L. Lohr, C. Escalante, M. Wetzstein. 2010. Food versus fuel: What do prices tell us? Energy Policy 38:445-451. ↩︎

Fargione, J., J. Hill, D. Tilman, S. Polasky, P. Hawthorne. 2008. Land clearing and the biofuel carbon debt. Science 319, 1235--1238 (2008).; Searchinger, T. et al., 2008. Use of US croplands for biofuels increases greenhouse gases through emissions from land-use change. Science 319, 1238--1240. ↩︎

Taheripour, F., W. E. Tyner, M. Q. Wang. 2011.Global land use changes due to the US cellulosic biofuel program simulated with the GTAP model. Argonne National Laboratory. [https://greet.es.anl.gov/publication-luc_ethano]l.; Dunn, J.B., S. Mueller, H. Kwon, M. Q. Wang. 2013. Land-use change and greenhouse gas emissions from corn and cellulosic ethanol. Biotechnology for Biofuels. 6, 51. ↩︎

Anderson, J.E., D.M. DiCicco, J.M. Ginder, U. Kramer, T.G. Leone, H.E. Raney-Pablo, T.J. Wallington. 2012. High octane number ethanol--gasoline blends: Quantifying the potential benefits in the United States, Fuel 97:585-594, ISSN 0016-2361, [https://doi.org/10.1016/j.fuel.2012.03.017]. ↩︎

Shahabuddin M., Alam M.T., Krishna B.B., Bhaskar T., Perkins G. 2020. A review on the production of renewable aviation fuels from the gasification of biomass and residual wastes. Bioresour Technol. 312:123596. [https://doi.org/10.1016/j.biortech.2020.123596]. ↩︎

Lynd, L. 2017. The grand challenge of cellulosic biofuels. Nat Biotechnol 35, 912--915. [https://doi.org/10.1038/nbt.3976]. ↩︎

National Academies of Sciences, Engineering, Medicine. 2016. Commercial Aircraft Propulsion and Energy Systems Research: Reducing the Global Carbon Emissions. Washington, D.C., The National Academies Press. [https://www.nap.edu/23490]. ↩︎

Díaz-Pérez M.A., Serrano-Ruiz J.C. 2020. Catalytic Production of Jet Fuels from Biomass. Molecules:25(4):802. [https://doi.org/10.3390/molecules25040802] ↩︎

"Renewable Fuel Pathways II Final Rule To Identify Additional Fuel Pathways Under Renewable Fuel Standard Program | US EPA". 2021. US EPA. [https://www]. [epa.gov/renewable-fuel-standard-program/renewable-fuel-pathways-ii-final-rule-identify-additional-fue]l. ↩︎

"Low Carbon Fuel Standard | California Air Resources Board". 2021. Ww2.Arb.Ca.Gov. [https://ww2.arb.ca.gov/our-work/programs/low-carbon-fuel-standard]. ↩︎

- ↩︎

Field J.L., L.R. Lynd, T.L. Richard, E.A.H. Smithwick, H. Cai, M.S. Laser, D.S. LeBauer, S.P. Long, K. Paustian, Z. Qin, J.J. Sheehan, P. Smith, M.Q.L. Wang. 2020. Robust paths to net greenhouse gas mitigation and negative emissions via advanced biofuels. Proceedings of the National Academy of Sciences 117 (36) 21968- 21977. [https://doi.org/10.1073/pnas.1920877117] ↩︎

Sanchez, D.L., N. Johnson, S.T. McCoy, P.A. Turner, K.J. Mach. 2018. Near-term deployment of carbon capture and sequestration from biorefineries in the United States. Proceedings of the National Academy of Sciences. 115, 4875--4880. [https://doi.org/10.1073/pnas.1719695115]. ↩︎

"Summit Carbon Solutions To Launch Major CCS Network To Reduce Carbon Footprint Of U.S. Biorefineries - Chemical Engineering". 2021. Chemical Engineering. [https://www.chemengonline.com/summit-carbon-solutions-to-launch-major-ccs-network-to-reduce-carbon-footprint-of-u-s-biorefineries/]. ↩︎

Field, et al., Robust paths to net greenhouse gas mitigation and negative emissions; Sanchez, D.L, J.H. Nelson, J. Johnston, A. Mileva, D.M. Kammen. 2015. Biomass enables the transition to a carbon-negative power system across western North America. Nature Climate Change. 5, 230--234. [https://doi.org/10.1038/] [nclimate2488]. ↩︎

"IPCC --- Intergovernmental Panel On Climate Change". 2021. Ipcc.Ch. [https://www.ipcc.ch/]. ↩︎

Field, et al., Robust paths to net greenhouse gas mitigation and negative emissions. ↩︎

Field, et al., Robust paths to net greenhouse gas mitigation and negative emissions; Griscom, B.W., Adams, J., Ellis, P.W., Houghton, R.A., Lomax, G., Miteva, D.A., Schlesinger, W.H., Shoch, D., Siikamäki, J.V., Smith, P., Woodbury, P., Zganjar, C., Blackman, A., Campari, J., Conant, R. T., Delgado, C., Elias, P., Gopalakrishna, T., Hamsik, M.R., Herrero, M., Kiesecker, J., Landis, E., Laestadius, L., Leavitt, S.M., Minnemeyer, S., Polasky, S., Potapov, P., Putz, F.E., Sanderman, J., Silvius, M., Wollenberg, E., & Fargione, J. 2017. Natural climate solutions. PNAS, 114(44), 11645-- 11650. [https://doi.org/10.1073/pnas.1710465114]. ↩︎

Owens, V.N. 2018. Sun Grant/DOE Regional Feedstock Partnership, Final Technical Report. E-Link Report/Product Number: DOE-SDSU-85041 [https://www.osti.gov/servlets/purl/1463330] ↩︎

Feyereisen, G.W., G.T.T. Camargo, R.E. Baxter, J.M. Baker and T.L. Richard. 2013. Cellulosic biofuel potential of a winter rye double crop across the U.S. corn- soybean belt. Agronomy Journal 105(3):631-642; Wolfe, M.L. and T.L. Richard. 2017. 21st century engineering for on-farm food-energy-water systems. Current Opinion in Chemical Engineering 18:69-76, [https://doi.org/10.1016/j.coche.2017.10.005]; Bonner, I.J., K.G. Cafferty, D.J. Muth Jr., M.D. Tomer, D.E. James, S.A. Porter, D.L. Karlen. 2014. Opportunities for energy crop production based on subfield scale distribution of profitability. Energies 7: 6509-6526, 10.3390/en7106509; Martinez-Feria, R.A., Basso, B. 2020. Unstable crop yields reveal opportunities for site-specific adaptations to climate variability. Sci Rep 10:2885. [https://doi]. [org/10.1038/s41598-020-59494-2]. ↩︎

Bonner, et al., Opportunities for energy crop production; Muth, D.J., 2014. Profitability versus environmental performance: are they competing? J Soil Water Conserv 69:203A-206A; M.E. Jarchow, M. Liebman, S. Dhungel, R. Dietzel, D. Sundberg, R.P. Anex, M.L. Thompson, T. Chua. 2015. Tradeoffs among agronomic, energetic, and environmental performance characteristics of corn and prairie bioenergy cropping systems. GCB Bioenergy 7: 57-71, 10.1111/gcbb.12096; X. Zhou, M.J. Helmers, H. Asbjornsen, R.K. Kolka, M.D. Tolmer, R.M. Cruz. 2014. Nutrient removal by prairie filter strips in agricultural landscapes. J Soil Water Conserv 69:54-64, 10.2489/jswc.69.1.54. ↩︎

Field, et al., Robust paths to net greenhouse gas mitigation and negative emissions. ↩︎

Ibid. ↩︎

Dale B. et al. 2016 "Biogasdoneright™: Food, Fuel and Environmental Services from Agriculture: An Innovative New System Is Commercialized in Italy" Biofuels, Bioproducts & Biorefining (2016); DOI: 10.1002/bbb.1671; Dale, B.E., Bozzetto, S., Couturier, C., Fabbri, C., Hilbert, J.A., Ong, R., Richard, T., Rossi, L., Thelen, K.D. and Woods, J. 2020. The potential for expanding sustainable biogas production and some possible impacts in specific countries. Biofuels, Bioprod. Bioref. 14:1335-1347. [https://doi.org/10.1002/bbb.2134]. ↩︎

Whittall, H. 2011. Proposal for an international ethical standard for biofuels. Biofuels 2(6): 607-609. [https://www.tandfonline.com/doi/abs/10.4155/bfs.11.112] ↩︎

International Energy Agency. 2019. Transport biofuels. In Renewables 2019: Analysis and forecast to 2024. ↩︎

- Europarl.Europa.Eu. [https://www.europarl.europa.eu/legislative-train/api/stages/report/current/theme/a-european-green-deal/file/revision-of-the-] [renewable-energy-directive].